Five years ahead of the 2030 target date set by the Global Methane Pledge for a 30% reduction in anthropogenic methane emissions, that goal remains more elusive than ever. A review of six of the largest emitters among signatory countries shows no sign of abatement just yet in aggregate. Key non-signatory countries aren’t doing any better. On the policy front, the two original sponsors of the Pledge are either stalling (in the case of the European Union) or backsliding (in that of the United States). Yet the picture is not uniformly gloomy and there are some hopeful developments coming from unexpected corners.

Delays in achieving the GMP goals makes the task ahead more daunting. The case for reducing emissions from this potent greenhouse gas is unquestionable. Methane has been responsible for nearly a third of global warming to date and is on track to cause half of the warming of the next 20 years. Lack of progress so far means that even steeper, faster emission cuts are now required. The longer it takes to reduce our footprint, the more heroic the cuts will need to be.

In this report, we extend our previous reviews to track developments over the past year. Using AI algorithms to analyze satellite data, we assessed annual methane emissions from 13 major fossil-fuel basins across nine key producing countries—six of which are signatories to the GMP. These countries were selected based on the scale of their fossil-fuel output and the availability of transparent, high-quality emissions data. They represent a broad cross-section of global production regions, including North America (the United States), the Middle East and North Africa (Iran, Iraq, Kuwait, and Algeria), Central Asia (Turkmenistan and Uzbekistan), Sub-Saharan Africa (South Africa), and Australia.

This year’s assessment captures the state of play at a pivotal moment. It reflects conditions in the final months of the pre-Trump era and sets the stage for the shifting political and industrial dynamics that have begun to emerge since January. The latest results highlight both the fragility of previous momentum and the potential for renewed direction in the years ahead. Our findings reveal where progress is accelerating, where it is stalling, and what these trends imply for the world’s ability to meet the GMP’s 2030 reduction goals.

Key Takeaways

-

- The bottom line: Emissions continue to rise. Between 2023 and 2024, aggregate methane emissions from the basins under review increased by 3.5%, continuing the trend of previous years. While some countries have stabilized or slightly reduced emissions since 2020, most large producers are still seeing growth. The gap between pledged ambition and actual delivery is widening. In aggregate, the GMP signatory countries under review are now 8.5% above their 2020 emission level. This lack of progress means that they now must collectively cut emissions by 35% versus 2024 levels, or 5.9% per year until 2030, to meet their goal.

-

- Oil exporting countries of the Arab Gulf stand out as an unexpected bright spot. Kuwait shows falling emissions in 2024, adding to other encouraging signs from its Gulf neighbors Saudi Arabia, the UAE, and Iraq. These large oil exporters—all of which are now GMP signatories—are emerging as regional leaders in methane performance, offering potential models for effective policy and operational reform.

-

- Phasing down coal production, especially by retiring older and deeper mines, brings strong methane co-benefits. Australia’s Bowen Basin, a large producer of both thermal and metallurgical coal, remains a relative bright spot in our survey, likely due to earlier mine closures, but more needs to be done to keep the momentum.

-

- Progress can be fragile. Reductions in emissions, once achieved, may not always ”stick”. Turkmenistan, a large methane emitter that had led our survey with sizeable emission cuts in 2022-2023, is a case in point: its emissions bounced back in 2024. Coming from a high base, this setback significantly worsened the average performance of our survey sample in 2024.

-

- The United States paradoxically remains a point of concern. Emissions in the three largest US tight oil and gas basins keep rising in absolute terms, though their methane intensity is edging lower. In aggregate, methane emissions from these basins increased by 18% from 2020 levels. On a brighter note, large operators in these basins appear to be taking methane abatement seriously, and smaller and less responsible ones may over time come under pressure to exit the business.

-

- All reductions in methane emissions are good, but some are not good enough. South Africa is an example of a country showing insufficient abatement progress: its emissions edged down in 2024 but remain too high to be on track to achieve the GMP goals.

-

- Western backsliding on methane abatement is an opportunity for others to take the lead. Neither China nor India – two of the world’s largest emitters – signed on to the GMP, yet both appear to be taking steps to reduce their large methane footprint. While beyond the scope of this year’s review, the trajectory of emissions in these countries will be critical to that of climate change, and as such warrants close monitoring.

- A new regulatory approach targeting chronic super-emitters looks promising. A “speed ticket” approach that would leverage independent satellite measurements to publicly expose major leaks would provide a low-cost and feasible way to accelerate accountability, reward leaders, and push laggards to act, driving direct and measurable results.

Methodology

Given the intermittency of large methane emissions, geospatial observation with monitoring satellites is the only scientifically robust and acceptable way to assess basin-level or regional emissions over a period of time. Occasional aerial surveys provide point-in-time information but it is not possible to extrapolate from them. In-situ sensors can detect small leaks but are not good at quantification, especially for large emissions, and cannot be deployed at scale.

Kayrros assessed basin-wide emissions from 13 major coal, oil and gas basins using basin inversions based on data from the TROPOspheric Monitoring Instrument (TROPOMI) on board the Sentinel-5 Precursor satellite, part of the European Space Agency’s Copernicus constellation. TROPOMI orbits Earth and takes frequent, detailed measurements of methane concentrations in the atmosphere. We use these measurements, along with other data such as wind patterns and known methane sinks, in complex mathematical models. These models “invert” the problem: instead of predicting methane concentrations from known emissions, they estimate emissions based on observed concentrations. A peer-reviewed description of the methodology was published in iScience in 2023 and can be found hier.

The basins under review were selected on two main criteria: the size of their production and the availability of high-quality, high-integrity TROPOMI data. We focus on fossil fuel emissions as an indicator of a country’s emission trajectory for two reasons: because of the large share of fossil fuels in overall man-made methane emissions; and because these emissions are highly concentrated and comparatively easy to abate, which has made them the main target of methane abatement policies to date.

Data uncertainty: It should be noted that our basin-inversion methodology may not always allow us to precisely identify the point sources responsible for the aggregated emissions that we set out to measure. Thus, emissions attributed to oil and gas basins may also include some emissions from co-located agricultural or waste-management facilities. Total emissions attributed to coal basins in Australia or South Africa may also include emissions from cattle farming in these areas or adjacent coalbed methane production facilities. This level of uncertainty is irrelevant to our overall assessment of the trajectory of methane emissions in these regions, however.

Methane Abatement Remains as Elusive as Ever

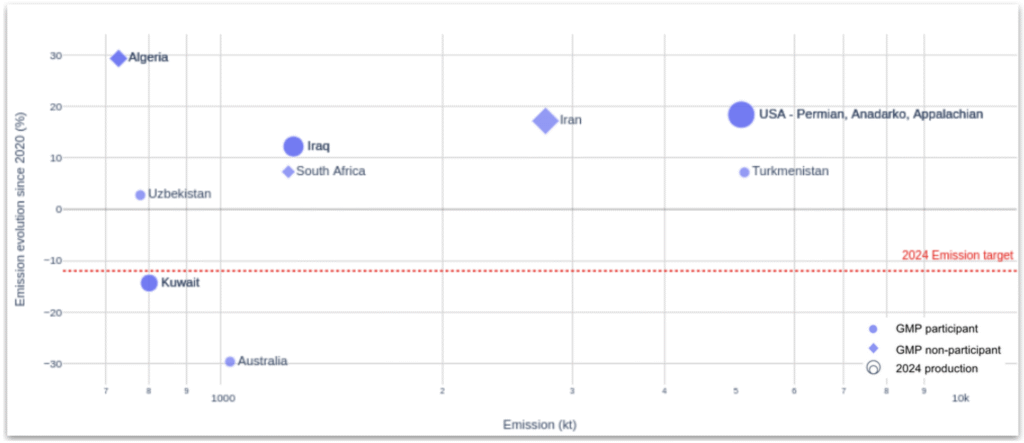

The goal of the pledge is slipping out of reach. In six GMP signatories that are collectively responsible for a large share of anthropogenic methane emissions(1), measured emissions ended 8.5% above 2020 levels. This means aggregate emissions from these economies will need to decline by 35% versus 2024 levels to reach the GMP target by 2030. Assuming linear progress, emissions would have to decline in aggregate 5.9% per year.

Despite a generally disappointing global picture, a handful of countries are showing meaningful progress toward the Global Methane Pledge (GMP) target of a 30% reduction in methane emissions by 2030 relative to 2020 levels. Among the 13 basins analyzed, Kuwait and Australia—both GMP signatories—stand out as the most promising performers.

Fig. 1 Change in annual methane emissions from fossil fuel basins, 2024 vs 2020

(1) The six countries account for 28% of anthropogenic emissions from GMP signatories, and 14% from global anthropogenic emissions based on IEA estimates.

The Bright Side: Gulf Producers as Abatement Leaders

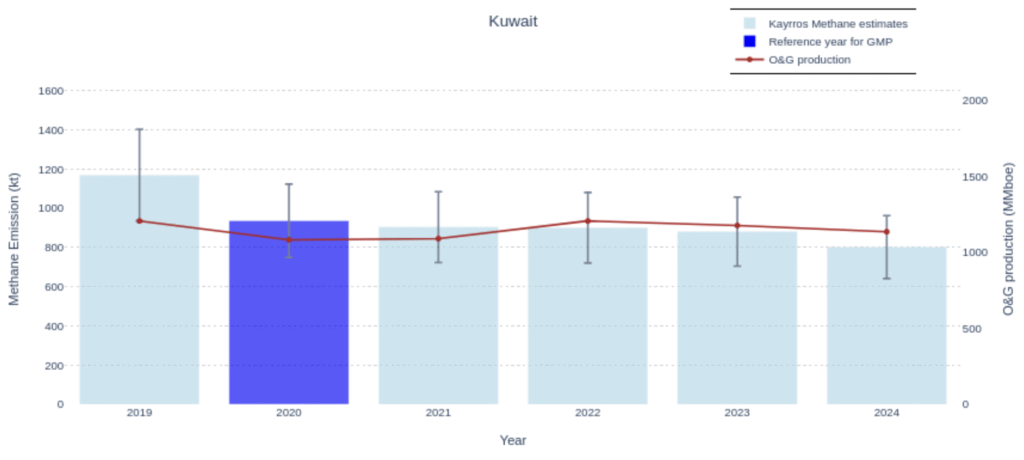

Kuwait’s progress is particularly encouraging and consistent with the improving trends observed across several Arab Gulf producers. In 2024, Kuwaiti oil and gas production edged down slightly, extending the modest decline seen in 2023. As in the previous year, methane emissions fell significantly faster than production. Compared to the 2020 baseline, Kuwait’s production remains higher, but its methane emissions are now markedly lower. This divergence between output and emission trends reflects tangible improvements in operational efficiency and leak mitigation.

Fig. 2 Annual methane emissions in Kuwait

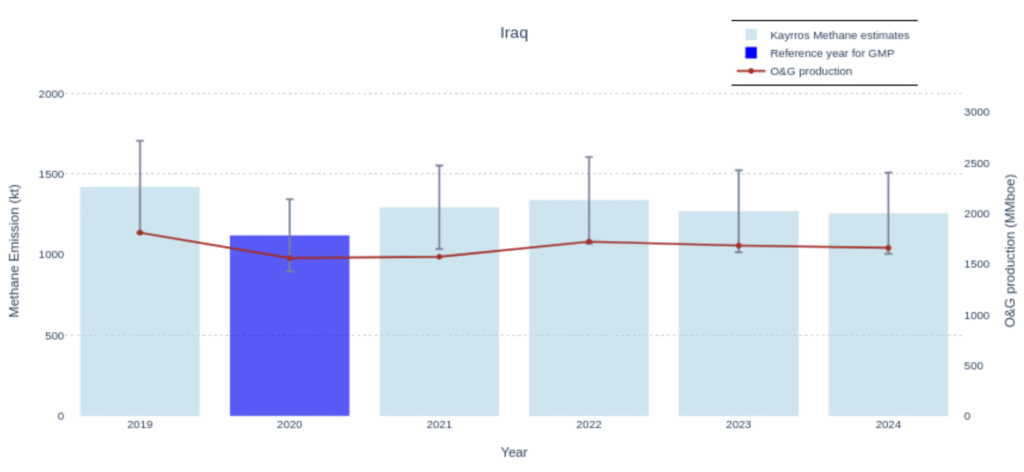

Iraq is also sending encouraging signals. Although still above 2020 levels, a year when they were exceptionally low, emissions have stabilized since 2022, and oil companies in the country are taking steps to reduce their footprint. Iraq presents one of the largest opportunities globally to reduce both methane and flaring, as it remains among the top three flaring countries in the world. Tackling these sources could deliver major benefits: lowering the country’s environmental footprint, improving public health, and providing valuable natural gas for oilfield activities and electricity generation, thereby reducing the need for diesel and imported gas. However, the key risk lies in replacing flaring with venting—a cheaper but far more damaging practice that has long been harder to detect and quantify. Such a shift would be rapidly visible in satellite data, though, underscoring the importance of transparent monitoring and international scrutiny to ensure genuine emissions reductions.

Fig. 3 Annual methane emissions in Southern Iraq

Other countries in the region that are not included in this study have shown either sustained good performance or notable improvement in their methane management practices. Saudi Arabia, the top OPEC oil producer, boasts of the second lowest methane intensity of all oil-producing countries (2). Despite expanding its oil and gas production, the UAE has managed to keep its methane intensity exceptionally low, among the lowest globally (3). Together, these countries are increasingly modeling best practices that could guide other major producers.

(2) Gasim et al., Comparing the Latest 2024 Estimates of Methane Emissions for Saudi Arabia. King Abdullah Petroleum Studies and Research Center, 2025.

(3) Gasim et al., Using Satellite Technology to Measure Methane Emissions in Arabian Gulf Countries. King Abdullah Petroleum Studies and Research Center, 2024.

Retiring Old Coal Mines Brings Methane Abatement Benefits

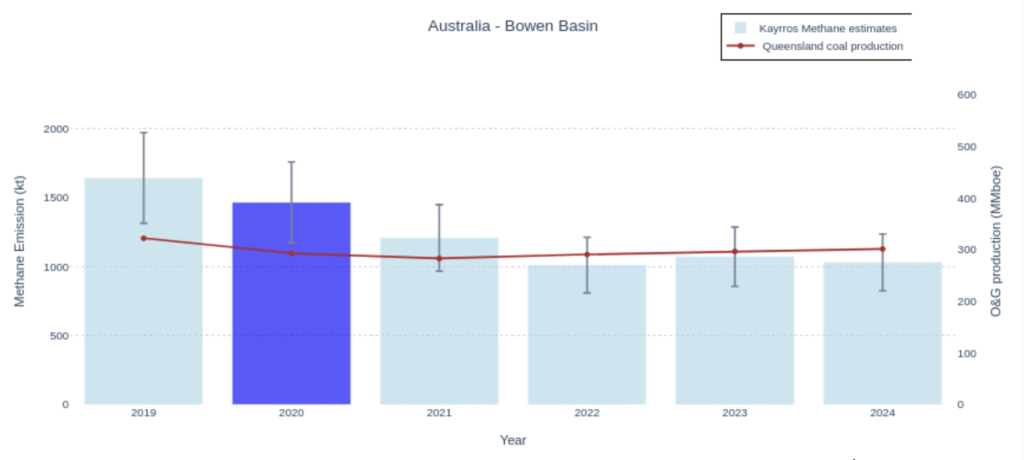

The coal sector is not only a top source of carbon emissions but is also associated with large methane emissions. These however are not unavoidable but, just as in the oil and gas industry, can be reduced with existing technology. A particularly efficient way to reduce coal mine methane is simply to retire older and deeper mines that are the most methane-intensive, however. Australia’s Bowen Basin illustrates this point.

The latest data shows that methane emissions from the Bowen Basin, while substantially above officially reported levels, remain well below 2020 levels, confirming the durability of the reductions achieved between 2019 and 2022. However, the absence of further declines in 2023 and 2024 suggests that most of these improvements were the result of mine closures and the decline of older, high-emitting assets, rather than of active policy intervention or new abatement measures. Nevertheless, the basin’s ability to maintain lower emissions amid steady production underscores the value of sustained operational vigilance and legacy asset management.

Fig. 4 Annual methane emissions in the Bowen Basin – Australia

A fundamental requirement for further progress is to start from an accurate inventory of current emission levels. Here, the picture from Australia is less rosy. A recent study (4) conducted by environmental NGO Ember Climate with Kayrros found that fugitive coal-mine methane emissions in Eastern Australia – a region that includes both the Bowen basin and the New South Wales basin, which together account for more than 90% of Australian coal production – were at least 40% higher than national estimates For a country whose metallurgical coal plays a critical role in global steel production, this gap raises both environmental and commercial risks. Strengthening measurement transparency would build on Australia’s abatement progress and help it communicate about its achievement in a trusted way. That in turn would reinforce confidence among international partners and help Australia maintain access to increasingly carbon-conscious markets such as the European Union.

(4) Wright, C., Setiawan, D., & Shannon, S. (2025). Satellite analysis identifies 40% more methane from Australian coal mines. Ember Climate. ember-energy.org

Cautionary Tale: National-Level Progress Can Be Fragile

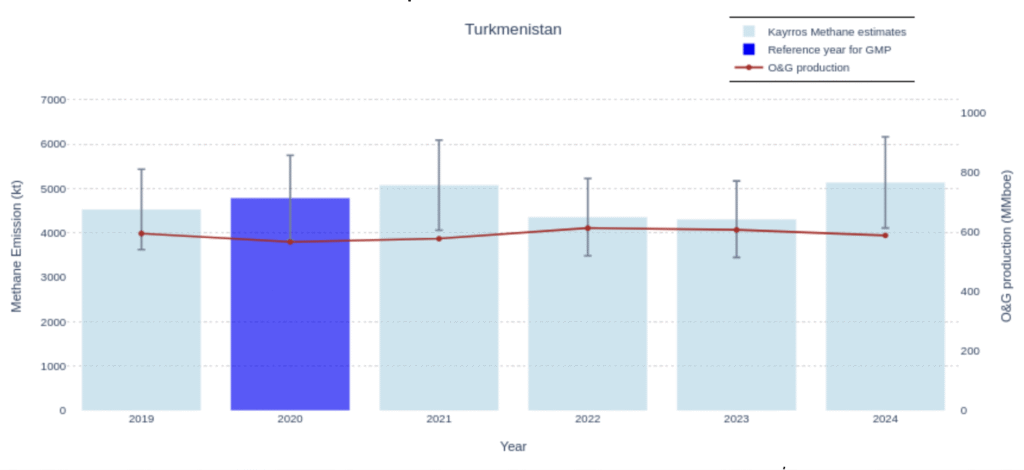

Turkmenistan, last year’s standout performer, experienced a sharp rebound in observed emissions in 2024—roughly a 19% increase year-on-year. The surge was led by the western, oil-producing basins, which reached an all-time high in methane emissions, while the eastern, gas-producing regions bounced back from relatively low 2022-2023 levels to a more typical range.

This steep rebound in Turkmenistan’s emissions raises questions about the sustainability of the latest reduction and its drivers: was the earlier dip due to lasting improvements to existing infrastructure that were then offset in 2024 by emissions from new sources, or did Turkmenistan hold its operations to higher and more responsible standards in 2022-2023, only to revert to its earlier ways later on? The broad trend remains one of volatile emissions linked to aging infrastructure, super-emitters tied to outdated venting practices, and chronic underinvestment in maintenance and leak detection. The see-saw pattern of the last years demonstrates that progress is achievable but does not necessarily stick. Let’s hope that 2024 turns out to be an outlier and that the country draws valuable lessons from it and redoubles its efforts to reduce its footprint.

Fig. 5 Annual methane emissions in Turkmenistan

Paradoxical Laggards: Methane Challenges in the U.S. and Uzbekistan

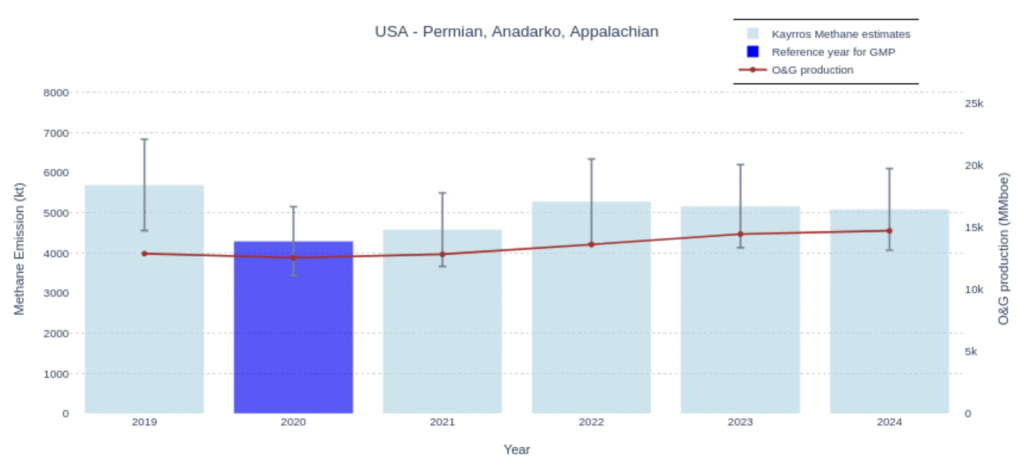

The United States, historically the main driver of the GMP, also failed to deliver significant emission reductions across the three basins analyzed—including the Permian Basin, the world’s most prolific oil field, the Anadarko and the gas-producing Appalachian. While overall production increased, methane intensity (emissions per unit of production) declined slightly, reflecting efficiency gains by larger operators. However, absolute emissions remain stubbornly high—around 18% above 2020 levels—making the U.S. one of the largest single sources of anthropogenic methane globally.

Fig. 6 Annual methane emissions in the Permian, Anadarko and Appalachian basins, U.S.A.

These results underscore the structural challenge of fragmentation in the U.S. oil and gas sector. Large companies have adopted advanced monitoring systems and invested in abatement technologies, but smaller producers—often operating under weaker regulatory oversight and tighter financial constraints—continue to lag behind. As the industry consolidates, there is potential for improved performance, yet this remains a gradual and uneven process.

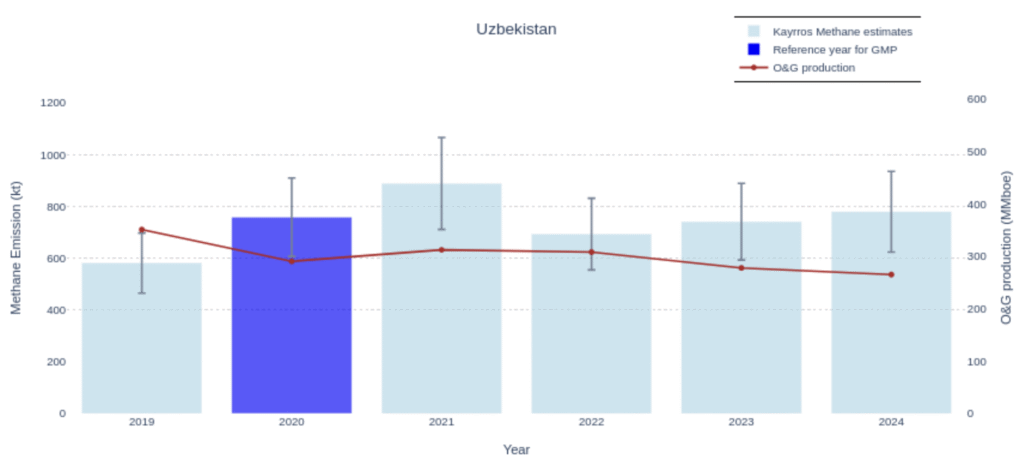

While the United States grapples with the challenge of reducing methane emissions amid rising production, Uzbekistan faces an equally perplexing situation: methane emissions from its oil and gas sector have climbed even as production has declined. Despite being rich in natural gas, Uzbekistan continues to face energy shortages as aging infrastructure and inefficiencies drive preventable methane losses. Uzbekistan had set ambitious goals for methane management, including the establishment of a national emissions inventory and a push to strengthen climate action across sectors like agriculture and waste. However, the gap between these commitments and actual progress highlights a broader challenge: translating policy aspirations into tangible results.

Fig. 7 Annual methane emissions in Uzbekistan

Non-Signatories on the Wrong Track

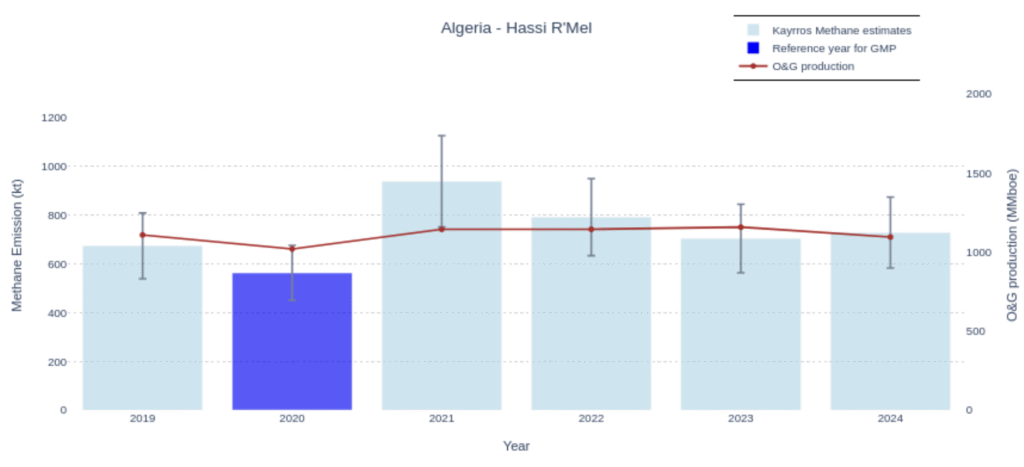

Algeria, a major gas exporter to Europe and a key player in Africa’s energy landscape, is one of the main fossil fuel producers that have yet to join the Global Methane Pledge. It is also a very large methane emitter.

In this report, we analyze methane emissions from Hassi R’Mel, a gas basin that is one of the country’s main methane hotspots. Following a sharp spike in 2021 as production rebounded from COVID-19 lows, methane emissions from the basin gradually declined in 2022 and 2023 and stabilized in 2024, but remain well above pre-COVID levels, let alone 2020 lows. Stubbornly high emissions from Hassi R’Mel mean that Algerian natural gas comes with a high methane intensity, which is potentially problematic given Algeria’s strategic position as a critical gas supplier to Europe, where demand for cleaner energy has risen.

Fig. 8 Annual methane emissions in Hassi R’Mel – Algeria

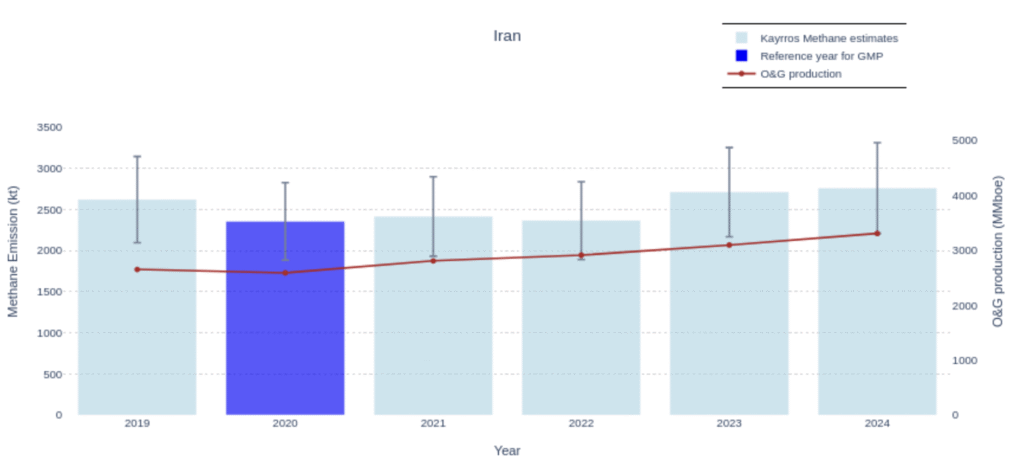

Iran saw a notable deterioration in its methane profile in 2024, extending earlier trends. Following an increase in oil production, methane emissions have risen sharply, largely tracking the growth in output. This increase underscores the challenge of balancing production gains with environmental performance in the absence of strong regulatory oversight.

Iran’s emissions outlook will likely depend on the dynamics of its export markets. Its crude is currently under international sanctions and its exports are limited to a very small group of countries. Should these buyers reduce their purchases, whether under the threat of secondary sanctions or for other reasons, Iran could be forced to curtail its production—potentially curbing emissions in the process.

Fig. 9 Annual methane emissions in Iran

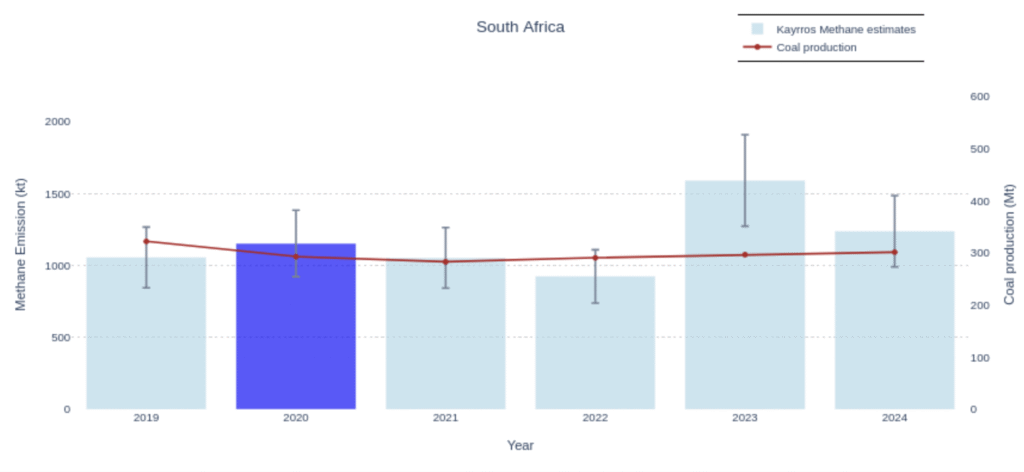

South Africa’s coal sector continues to lag in methane reduction. Despite a slight decline in emissions in 2024 from the high levels of the previous year, progress remains insufficient. Without stronger policies or infrastructure investments, the country’s reliance on coal risks locking in high methane levels for years to come.

Fig. 10 Annual methane emissions in South Africa largest coal basin

Methane Policy Shifts to the East

Looking beyond the period under consideration in this survey, the policy landscape has been in flux since early-2025. The return of Donald J. Trump to the U.S. presidency marks a shift away from the methane-focused agenda of the previous administration. Since taking office, the new administration has systematically rolled back key Biden-era climate regulations, notably as regards methane abatement, easing the pressure on U.S. companies to reduce emissions. At the same time, Washington has pressed the European Union to soften its own stance, weakening what had been a strong transatlantic alignment on methane policy.

Kayrros data suggest that even before this political shift, the impact of Biden-era methane policies had been limited, however. Emissions from major U.S. basins were already trending upward, raising doubts about the overall effectiveness of the GMP framework. In that sense, the current rollback may be less consequential than it appears, revealing deeper challenges in how methane reduction policies are designed and implemented.

With the U.S. and EU stepping back from the vanguard, but stubbornly high methane emissions continuing to pose an elevated climate risk, there is both a need for alternative abatement pathways and an opportunity for other countries to step up to the plate. Two countries of particular interest are China and India—the world’s two most populous nations and major emitters, each now charting a more independent policy course. Following the U.S. withdrawal from the Paris Climate Accord in January 2025, China has reinforced its climate policy, strengthening its Net Zero commitment with updated decarbonization targets and positioning itself as a global climate leader. In a video statement to the UN in New York, President Xi Jinping in September 2025 said that China would reduce its greenhouse gas emissions across the economy by 7-10% by 2035, while “striving to do better” (5). While methane is not yet a central focus, China’s coal phase-out plans are anticipated to deliver meaningful climate co-benefits. Nonetheless, far greater reductions could be realized if methane abatement were elevated as a policy priority. China also has launched several methane-tracking satellites, and enjoys advanced satellite image processing capability. Its Gaofen-5, Ziyuan-1, and Huanjing-2 constellations participated in the latest Stanford-controlled release study (Sherwin et al., 2024) underscoring the maturity of China’s remote sensing capabilities. The launch of Xiguang-1, the nation’s first commercial high-resolution satellite for point-source methane monitoring, not only addresses a key gap in domestic commercial methane monitoring but also positions China as an emerging leader in global methane observation and greenhouse gas governance.

India, meanwhile, faces a different challenge: its large share of methane emissions comes predominantly from landfills and agriculture. Efforts to tackle these sources could yield major co-benefits for public health, urban air quality, energy import costs and access to modern energy services. Encouragingly, India has begun to roll out policy measures supporting methane capture and waste-to-energy programs, signaling early but promising momentum.

In addition to moving geographically from “Western” advanced economies to the East and South, the impetus for methane abatement is also shifting from the public to the private sector. The fossil fuel industry is showing that it can be a critical force for progress. The financial sector is increasingly building methane performance standards into its strategic objectives and work practices. Across the Gulf, the United States, and other regions, major oil and gas companies are increasingly embracing satellite-based methane monitoring, improving transparency and accountability. As market conditions favor further industry consolidation, the influence of large best-in-class operators is growing—potentially accelerating methane reductions even in the absence of strong regulatory drivers. Ultimately, the path forward depends on sustained industry engagement, backed by transparent data and credible measurement systems.

(5) Poynting, M. (2025 September, 24). China makes landmark pledge to cut its climate emissions. BBC. https://www.bbc.com/news/articles/cj4y159190go

Silver Lining: The Rise of Geospatial Adoption

Geospatial methane-monitoring technologies are getting more broadly adopted. This is one of the most hopeful developments affecting methane action today. Countries and companies that were once reluctant to embrace earth-observation technologies or pushing back against satellite measurements of higher methane emissions than they reported are increasingly willing to adopt these technologies and accept their findings.

California’s $100 million satellite initiative shows how local leadership can drive progress even when national action stalls, enabling real-time detection and public reporting of emissions. At the global level, the International Methane Emissions Observatory’s Methane Alert and Response System (MARS) is expanding its reach, helping countries act on verified emissions data and creating a new norm of accountability.

Industry, too, is changing. Partnerships like ExxonMobil’s work with GHGSat and Kayrros’s collaborations across the Middle East signal that methane monitoring is becoming a strategic asset, not just a compliance exercise.

Growing adoption of earth-observation technologies today sets the stage for faster and more effective abatement tomorrow. This is one of our best hopes of making up for lost time and delivering on the GMP goals.

From Pledges to Accountability: Initiating a Methane ‘Speed Ticket’ Mechanism

The global methane challenge is no longer one of awareness or detection and measurement technology. Despite encouraging signs of progress in many areas, it remains fundamentally one of implementation and regulation. As the Global Methane Pledge reaches its midpoint, progress is real but punctual and fragmented: leaders have emerged, yet their achievements are overshadowed by a handful of massive, preventable leaks. Each large emitter can erase the annual gains of dozens of responsible producers. They distort global statistics, blur success, and fuel the perception that collective climate action is failing.

To move forward, methane accountability must become institutionalized and systematic. A “speed ticket” mechanism, inspired by road-safety enforcement but adapted to climate governance, could make that possible. Using existing satellite data, it would identify and publicly flag major methane releases in near-real time. No monetary fine, no sanction, only evidence that the world is watching. Visibility alone can be transformative: reputational pressure works faster than regulation, and transparency can drive behavior where policy still hesitates. This approach would reward those already leading by example, while isolating chronic emitters who undermine collective credibility. More importantly, it would create a new dynamic of measurable progress.

Super-emitters, though only the tip of the iceberg, are the ideal focus. They are simple to monitor and offer the most immediate, cost-effective abatement opportunities, but they also reveal something deeper: the operational discipline and efficiency of an operator. A company that takes steps to prevent major emission events will naturally strengthen its leak management systems across the board, improving performance well beyond the initial fix. Thus, targeting super-emitters not only delivers rapid, measurable reductions, it raises the bar for operational excellence industry-wide.

Implementing such a system would be remarkably easy and low-cost: the data already exist, and the tools are operational. In contrast, determining the precise methane or carbon intensity of an asset or company remains technically complex, inconsistent across jurisdictions, and not realistically accurate in the near term. A “speed ticket” approach would cut through that uncertainty by focusing on what can be seen, verified, and acted upon now.

If the first half of the Global Methane Pledge was about promises, the second must be about proof. The ‘speed ticket’ concept can help bridge that gap, turning invisible emissions into visible progress, and pledges into performance.