Is the long-awaited wall of LNG supply finally on its way?

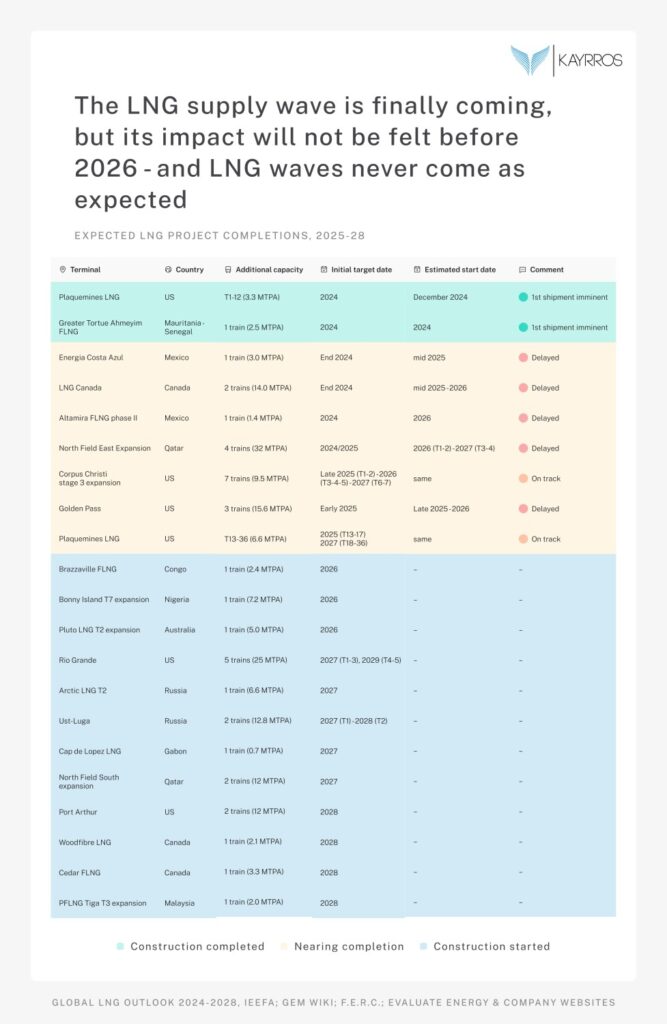

- Satellite monitoring shows new LNG trains around the world are finally making progress. Yet despite many projects being scheduled to start up in 2025, the real impact of the LNG wave will not be felt before 2026.

- The world’s top two players, Qatar and the US, are well ahead of the pack, further consolidating their market dominance.

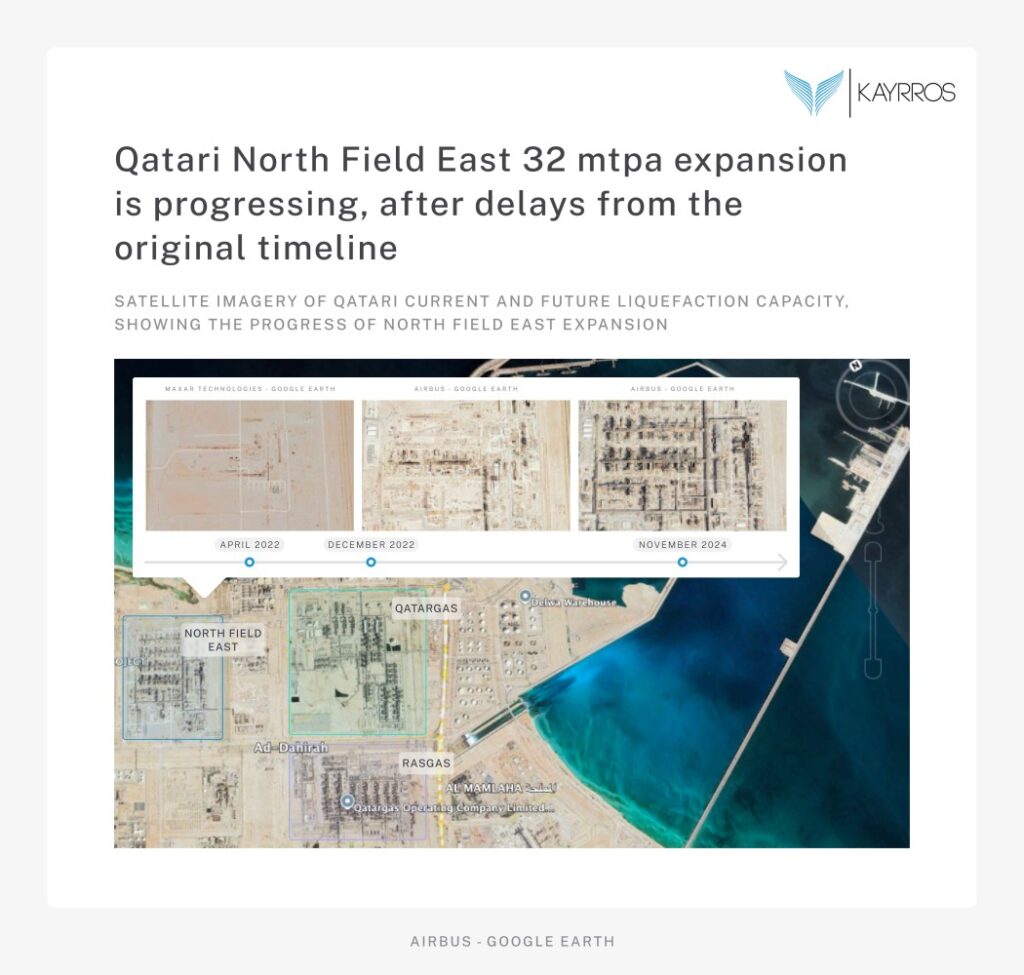

- In Qatar, phase one of the 64 mtpa North Field East project is quickly moving ahead, but completion and commissioning of the project, which is adjacent to RasGas and Qatargas, remain months away, satellite imagery reveals. Project owner QatarEnergy has kept conspicuously quiet about the status of its construction projects.

- Elsewhere, Mexico and Canada are emerging as substantial new sources of supply, while Africa is also expanding capacity.

- The long awaited LNG tsunami which forecasters had been expecting to flip tight LNG balances to oversupplyand bring prices crashing down has proved elusive. Chronic delays have lifted prices even as international sanctions have kept Russian piped gas largely off-limits to Western markets.

- A key question facing global natural gas marketsis whether a resolution of the conflict between Russia and Ukraine pushed by Washington could bring Russian supply back to Europe before new LNG production comes online.

- As global gas markets continue to face uncertainty, and with the potential for further delays remaining high, the need for near-realtime monitoring is more acute than ever.

- Qatar, whose position as the world’s #1 LNG exporter was overtaken by the US in 2023, is planning an 84% expansion of its LNG production capacity via the multi-phase North Field Expansion project.

- Altogether, North Field Expansion will bring 64 mtpa of new capacity by 2030, liftting the country’s total production capacity to a whopping 140 mtpa.

- Yet the project has suffered delays, Phases I and II of North Field East are now expected to collectively add 32 mtpa capacity in 2026 and 2027.

- This marks a significant delay from the original 2025/2026 timeline.

- Partially offsetting construction delays, Qatar this year has been deviating from its usual production schedule and appears to have been postponing spring maintenance, with all trains currently running, Kayrros analysis reveals.

- Kayrros geospatial intelligence is an essential source of insights into Qatari LNG, including both construction and operations.

- Given the pace of construction, Kayrros expects Qatari North Field East Expansion to match the updated timeline – delayed from the original 2025 timeline for Phase I.

- Canada LNG missed its original timeline, with the first cargo now expected in July 2025.

- Supply impact from Golden Pass is not expected to be felt in the market before 2026, Kayrros analysis of satellite data shows. This compares with an initial target of 2025. The bankruptcy of the project’s lead contractor in May 2024 negatively affected its timeline.

- This means the LNG supply wave is expected to have a material impact on the global balance in 2026 only, delayed from 2025.

- It is not the first time this impact is delayed, and there is still a significant risk of further delays.

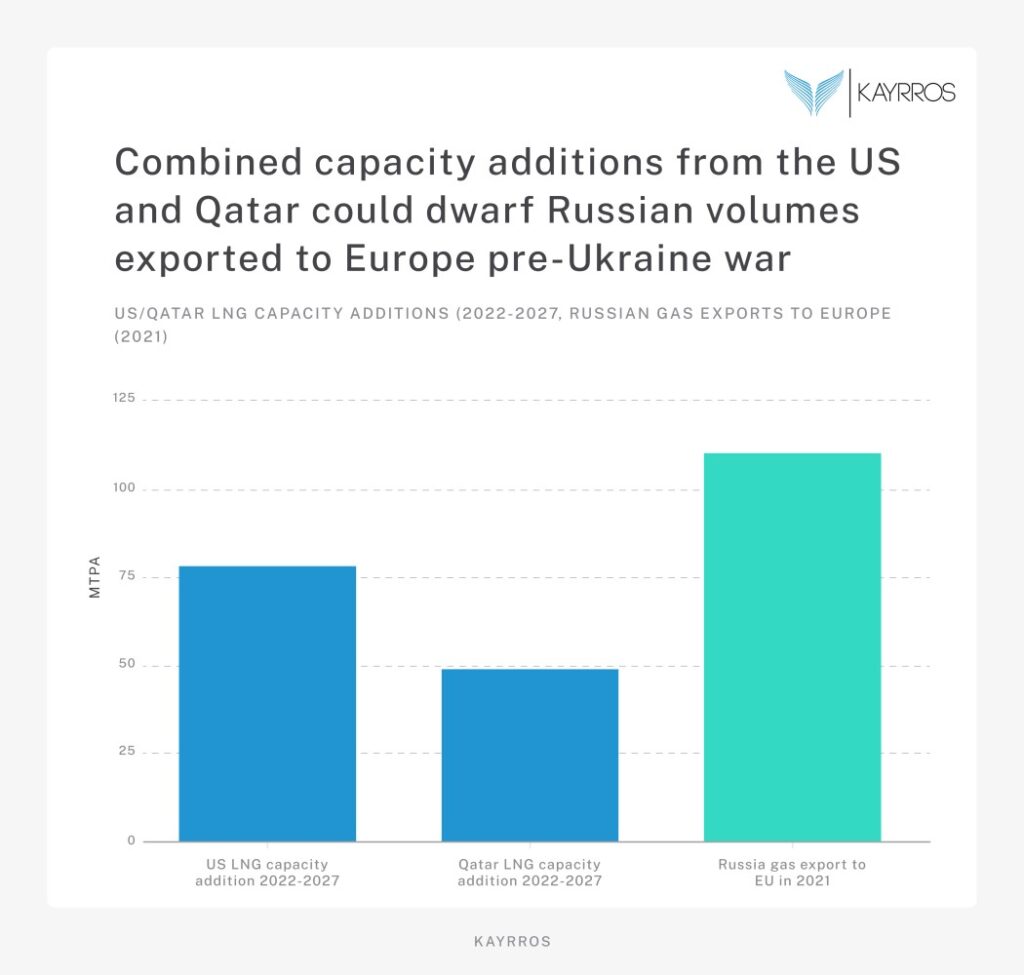

- Collectively, Qatar and the US are expected to add 126 Mtpa of incremental liquefaction capacity by 2027from levels prior to the invasion of Ukraine. This compares with Russian gas exports to Europe of 110 Mtpa in 2021, the year prior to the invasion.

- On paper, incremental US and Qatari capacity comfortably offsets Russian supply losses, and more. This appearance of balance conceals steep upside and downside risks to the market depending on timing and geopolitical context, however.

- On the one hand, the full supply increment is not expected to come online before 2027, leaving significant shortfall risks if Russian exports to Europe remain off the market and demand is robust.

- On the other hand, new production capacity could trigger an oversupply challenge if Russia resumed westward exports and demand growth proved underwhelming. A price collapse could be very challenging indeed for higher-cost producers in the US and elsewhere, though it would presumably turbocharge US efforts to reshore manufacturing while also helping to bring down inflation.

In the news

- Louisiana’s Haynesville shale basin activity boosted by rising demand from LNG (Reuters).

-

China’s Q1 2025 LNG imports at a seasonal 7-year low. (Bloomberg).

-

LNG projected to meet the largest share of global gas demand growth expected by 2040. (Shell)